New Palo Alto, better Palo Alto, closer Palo Alto

Hello, and welcome to this week's Unzip.Media newsletter!

I generally cringe when I hear that people working in European tech should adopt the US way of thinking and acting: from working longer hours, to abolishing employee protections, to being less humble and going over the top with self-promotion. (As a journalist, I'd much rather deal with a founder who is too modest than sift through a pile of fake-it-till-you-make-it kind of bullshit — but that's a matter of personal preference, I suppose.)

I do, however, see one aspect of the way people from North America think that we might want to internalise in Europe — and it has to do with the perception of distances, as in what's far and what's close. It might be quite relevant for the issues the ecosystem has to solve, and here's how.

Ever since I began writing about European tech startups — that'd be about 15 years now — journalists and analysts have been comparing the continent's ecosystem with that of either the US as a whole, or Silicon Valley. But the comparison always felt off somehow, as the markets and geography are too different in both cases.

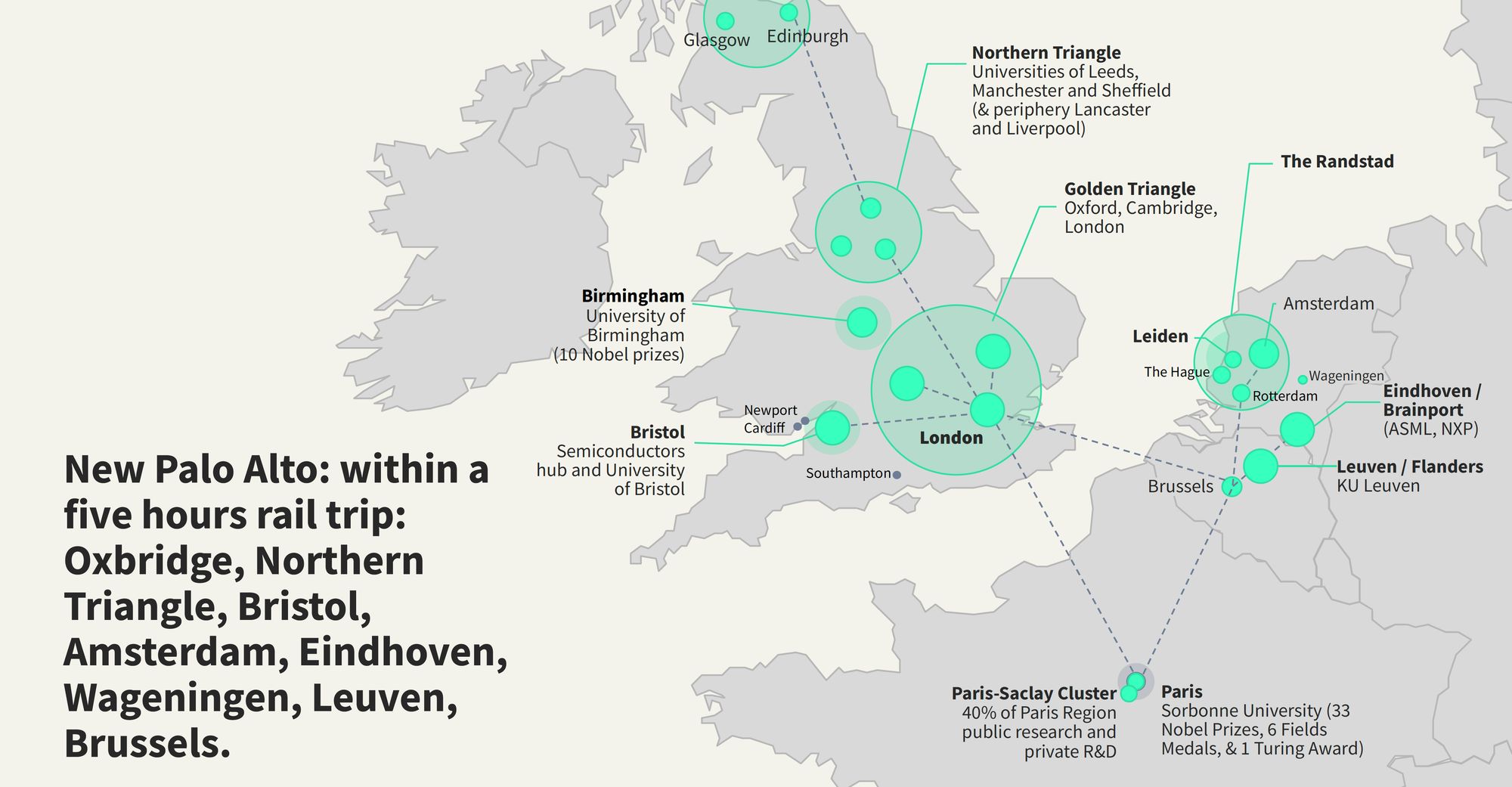

Now, I think there's a better and more helpful way to think about both this comparison and the European ecosystem and its parts. A few weeks ago, I had a chance to talk to three very smart people about the concept of the New Palo Alto (NPA) — a European supercluster ecosystem, which is much more comparable to Silicon Valley in terms of geography and innovation density than Europe as a whole.

Defined as an area roughly within a five-hour train ride from London, NPA includes the tech hotspots in the UK (London, Oxbridge, The North, etc.), Paris, Brussels, and the hubs like Eindhoven and the Randstad area. (I also wonder why the Wadden Islands are missing from the map above.)

Together with Orla Browne (Dealroom), Constantijn van Oranje (Techleap.nl), and Saul Klein (LocalGlobe and Phoenix Court), we spent over an hour going through a trove of data that shows how the cluster has been performing, where it's still lacking, and what are the areas in which we're actually doing better than our overseas counterparts.

It's not the point of this newsletter to list everything (the list is long!) — but do check out the full video, I enjoyed this conversation thoroughly:

With the idea of NPA established, let's go back to the distance perception issue I opened this newsletter with. I think the ecosystem would greatly benefit if its members were to view a trip from, say, Amsterdam to Paris or London as a quick local outing (it only takes three to four hours after all), and hence see those cities as being basically next door from each other. I'm talking here first and foremost about both founders and early-stage VCs.

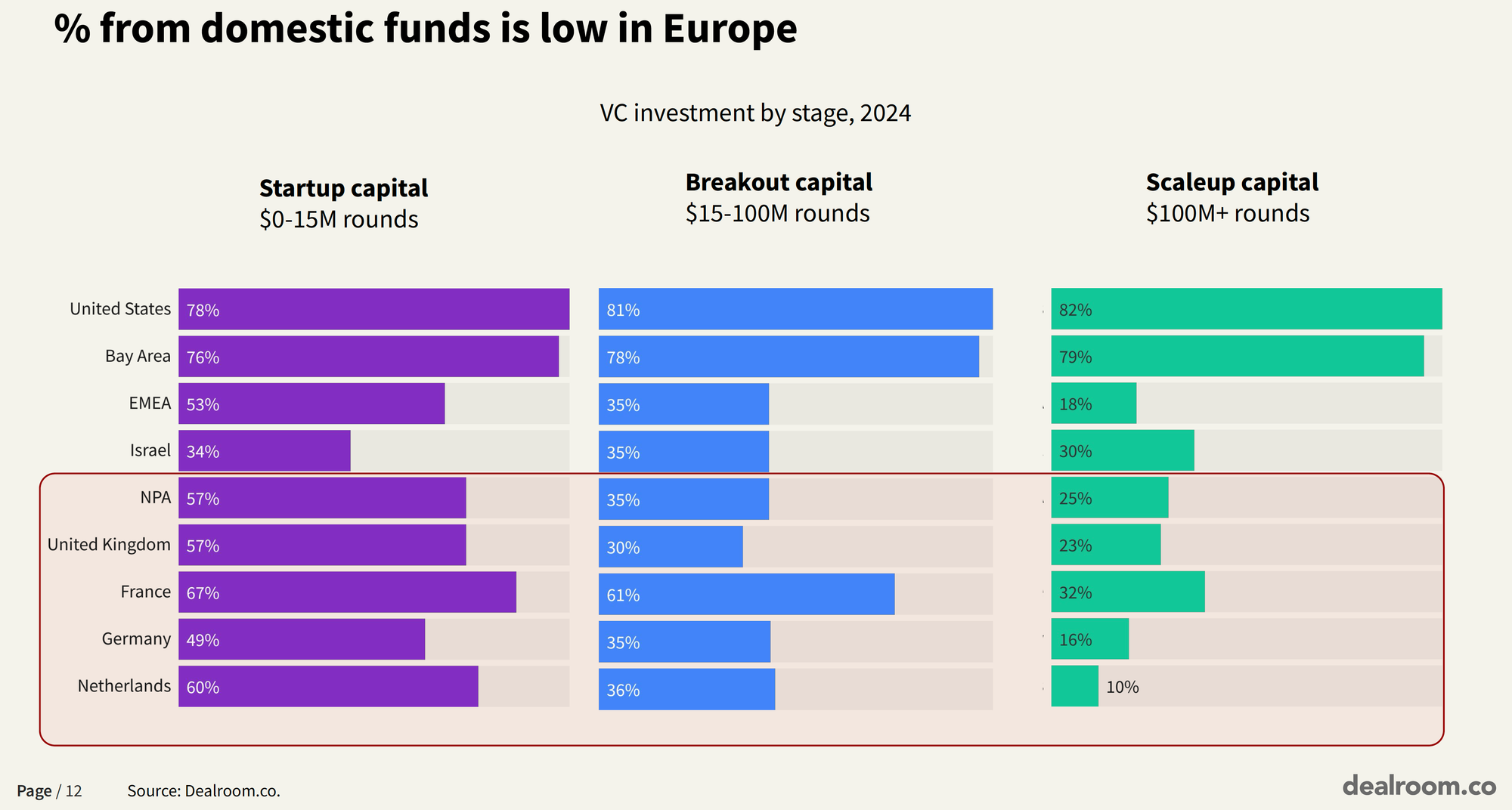

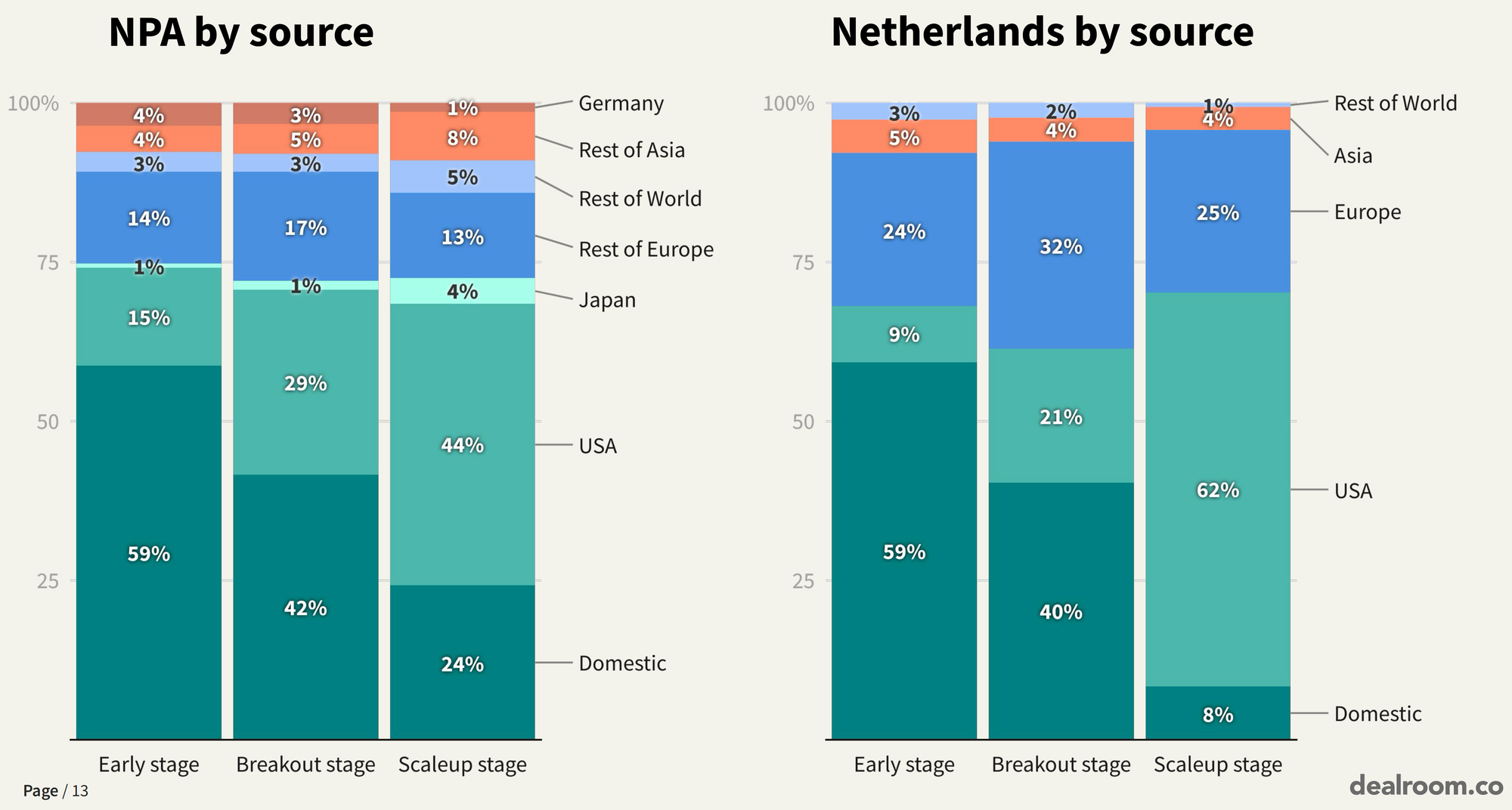

The kind of distance perception that expands the understanding of a local area would help with making connections across the ecosystem and potentially help solving one of the issues discussed in the video above: that a huge chunk of startup funding in NPA comes from elsewhere. The shares of non-domestic capital range from 43% at the startup stage (<$15 million) to 75% (!) for rounds over $100 million, compared to 22% and 18%, respectively, in the US. Here are two relevant slides:

An interesting thing I see in the graphs above is that the percentages of domestic funding for NPA and individual countries (the UK, the Netherlands, and France) at the startup stage are very close. Therefore, “domestic funding” in the case of NPA actually still means that early-stage startups are mostly raising within their own countries rather than cross-border.

I believe that by expanding the area that's considered local we can improve these numbers, at least for smaller rounds (which we have plenty of capital for, unlike the breakout and scaleup stages). This change in perception, in my view, could break the pattern I've observed for founders to either raise domestically or reach out to US investors. I'd say halving the percentage of US-originated funding from the graphs above would be a success.

Of course there are many more reasons for this situation than simple geographic perception, from local regulations and bureaucracy to market fragmentation and language barriers to the general state of European capital markets. Fortunately, at least the regulatory part is being dealt with by EU Inc., numerous policymakers, data crunchers, and VCs — including my conversation partners from the video above. But changing what we consider our home ecosystem feels like a good place to start for most of us that doesn't require an entire movement.

And this is it for this week's edition!

Before signing off, I'm happy to report that this newsletter has reached 600 subscribers on LinkedIn and the Unzip.Media website itself — big thanks to everyone reading these notes! Any and all feedback is very welcome at andrii@unzip.media — don't hesitate to reach out!

If you know someone who could enjoy this newsletter, do share it with them — that'd mean the world to me.

Until next time,

Andrii.